The $114 Billion Fortress: Unmasking the Structural Mispricing and Hidden Casualty Risks Inside Chubb Limited. [Part1/3]

A forensic deconstruction of the world's largest publicly traded P&C insurer reveals an underlying tension between record cash generation, expanding margins, and masked long-tail reserving risks.

Company: Chubb Limited

Ticker: CB

Exchange: NYSE

Closing Price: $323.40

Date: June 20, 2026

Regulatory Compliance & Publisher’s Exemption Notice:

This publication is strictly for educational and informational purposes. The data and forensic modeling presented reflect an objective analysis of historical statutory filings, including cross-border MD&A and insider flow data. This briefing does not constitute personalized financial, investment, or trading advice. No recommendations are made to buy, sell, or hold any security. Past performance is not indicative of future results.

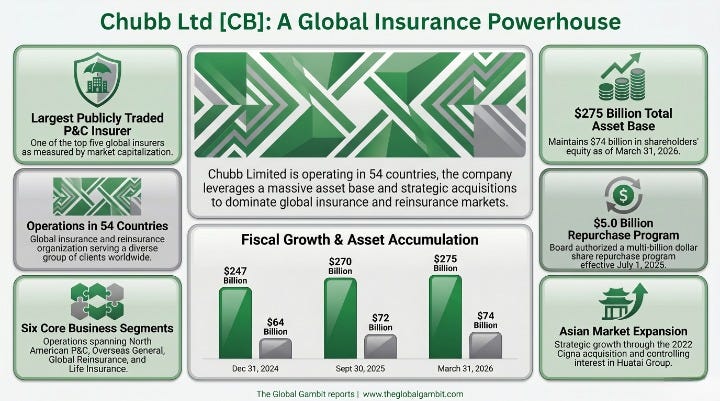

Market sentiment currently frames Chubb Limited as an impenetrable fortress of global underwriting discipline. Over the trailing twenty-four months, the equity has been propelled by robust capital return programs and the historic consolidation of its Asian assets.

However, a quantitative extraction of the underlying statutory data reveals a divergence from the headline consensus. When we bypass the polished investor presentations and cross-reference the granular footnote archaeology in The $114 Billion Fortress_ Unmasking the Structural Mispricing and Hidden Casualty Risks Inside Chubb Limited, an entirely different operational reality takes shape.

While the C-suite touts record top-line expansion, the underlying prior-period reserve developments and unrealized fixed-maturity losses indicate emerging duration mismatches and long-tail casualty deterioration. The data suggests this is a structural catalyst the broader market has yet to fully price in.

The Forensic Roadmap: Deconstructing the Chubb (CB) Engine

The sheer scale, geographic dispersion, and balance sheet complexity of Chubb Limited necessitate a comprehensive forensic breakdown to objectively evaluate its intrinsic valuation and historical compounding metrics.

Part 1 (Current Briefing): Deconstructs the core business segments, the holding company revenue architecture, the structural economic moat, and the C-suite capital allocation philosophy.

Part 2: Executes a deep-dive margin forensic analysis, tracking the exact operational drivers propelling recent combined ratio compression.

Part 3: Investigates the terminal risks and provides a multi-scenario intrinsic valuation model utilizing a residual income framework.

[PAYWALL CUTOFF] The remainder of this forensic deep-dive—including the breakdown of the $170 billion float, the 6 core operating segments, the "10% Rule" governance moat, and the executive compensation red flags—is reserved for Logic & Leverage premium subscribers. Upgrade your access below to analyze the structural risks threatening this compounder.