The Silent Catalyst Missing from Woodside Energy (WDS)

Beneath the passive income allure, regulatory filings reveal a stark contrast between institutional yield-chasing and executive distribution.

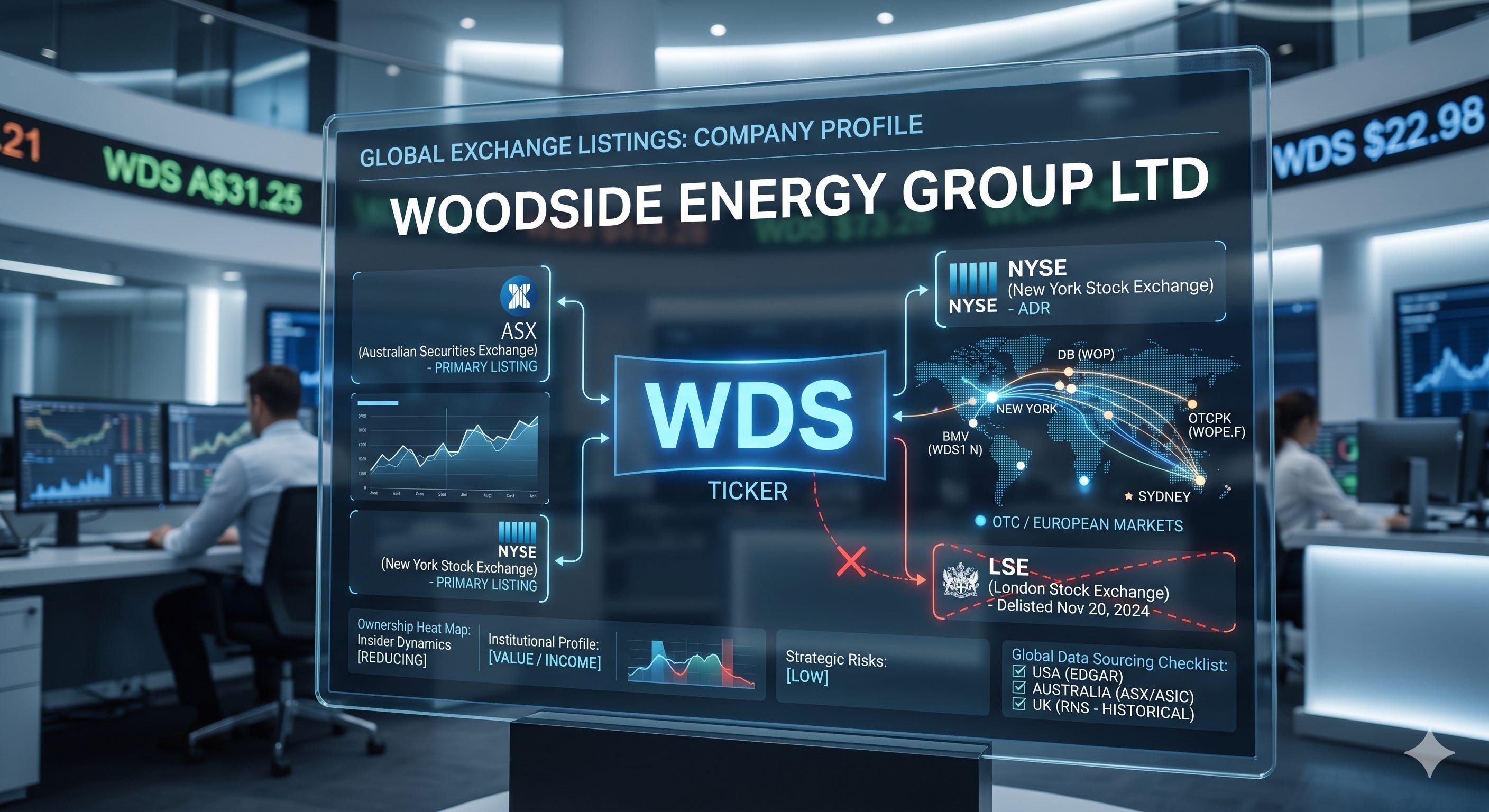

Woodside Energy Group Ltd

Exchange Listings: ASX: WDS (Primary) | NYSE: WDS (ADR)

Closing Price (as of Friday, May 15, 2026): ASX: A$31.25 | NYSE: $22.98

Disclaimer: The following intelligence briefing is for educational and informational purposes only. It does not constitute financial advice, nor is it a recommendation to buy, sell, or hold any security. …