Tracking the Smart Money: Why Insiders Are Quietly Backing Adobe Inc at Multi-Year Lows

A forensic breakdown of the narrative panic, the $25B buyback weapon, and why institutional fund managers are stepping in at a ridiculous 8x forward P/E. (Short Read)

Why the Market Panic Happened

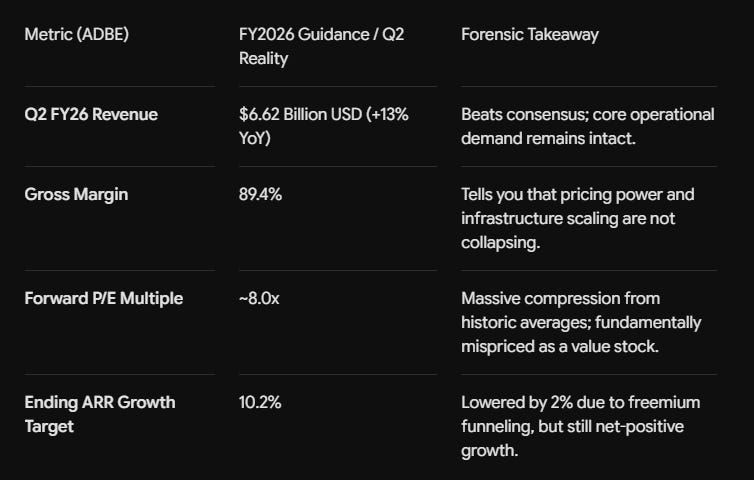

To understand the buy side at $194 USD, we must first look at what caused the vertical drop from the $260 USD handle down to current multi-year lows. The market did not sell off on current earnings; it sold off on structural uncertainty buried in the recent Q2 FY2026 disclosures.

The Management Vacuum: Long-time CEO Shantanu Narayen announced his planned retirement in March 2026. Compounding this, alongside the Q2 print on June 11, CFO Dan Durn abruptly announced his departure to join Marvell Technology. Entering H2 2026 with a dual-vacancy at both CEO and CFO introduces execution risk that quantitative algorithms immediately penalize.

The Freemium Pivot & ARR Sacrifice: Adobe downgraded its organic FY2026 Annualized Recurring Revenue (ARR) growth guidance by roughly 2 percentage points. To combat low-cost AI competition, management chose to defer planned Creative Cloud price hikes (”line optimizations”) and redirect traffic into free tiers for Acrobat, Express, and Firefly. The market interpreted this guide-down as a loss of pricing power rather than a long-term customer acquisition strategy.

The “AI Eats Software” Narrative: Sentiment hit rock bottom following the April 2026 launch of Anthropic’s Claude Design, alongside scaling capabilities from Canva and Figma. The prevailing narrative is that generative AI tools will compress seat licenses and eventually cannibalize Photoshop and Illustrator subscriptions.

The Institutional Long Case: Why Value Managers Are Stepping In

While momentum capital is fleeing, institutional fund managers and forensic analysts are buying the narrative capitulation because the underlying fundamentals have decoupled from the price.

1. Unprecedented Valuation Disconnect

Adobe has historically traded at a trailing P/E multiple of 30x to 40x. At $194 USD, on raised FY2026 non-GAAP EPS guidance of $24.35 USD to $24.45 USD, ADBE is trading at a forward P/E of just ~8x, and a trailing P/E of roughly 11x. This places a high-margin tech monopoly at a cheaper multiple than generic brick-and-mortar legacy companies, creating a deep margin of safety.

2. The $25 Billion USD Buyback Weapon

On April 21, 2026, Adobe’s board authorized a fresh $25 billion USD share repurchase program through April 2030. At current depressed levels, Adobe’s total market cap has shrunk to roughly $78 billion–$80 billion USD.

With $25 billion USD in authorization, Adobe has the capacity to buy back and retire up to 30% to 32% of its entire outstanding share float at these prices. This creates an incredibly hard structural floor for EPS accretion, regardless of top-line deceleration.

3. Misunderstood AI Monetization

The narrative says AI is killing Adobe, but the actual 10-Q data reveals the opposite. Adobe’s AI-first ARR tripled year-over-year to crack $500 million USD, and total AI-influenced ARR now represents over one-third of their entire active book of business. They are effectively cross-selling AI credits to existing enterprise users.

Upcoming Turnaround Catalysts

Fund managers building stakes at $194 USD are looking toward three distinct catalysts to reverse the negative sentiment over the next 6 to 12 months:

C-Suite Resolution: The primary near-term catalyst will be the formal announcement of a permanent CEO and CFO. The board has indicated a desire to have a new CEO in place to lay out the FY2027 strategic plan. Stabilizing leadership removes the “uncertainty premium” currently discounting the equity.

The Topaz Labs Integration: Adobe recently announced the strategic acquisition of Topaz Labs, an Emmy-winning AI firm specializing in professional-grade photo and video enhancement. Integrating Topaz’s localized, desktop-heavy AI processing into Creative Cloud shores up Adobe’s defenses against purely cloud-native AI startups, defending the high-end professional moat.

Freemium Conversion Proof-of-Concept: By late Q4 FY2026 or early FY2027, the initial cohorts onboarded via the new friction-free free tiers (Express and Firefly) will hit conversion milestones. If Adobe can demonstrate a predictable conversion rate from free users to paid tiers, the market will re-rate the freemium pivot from an “act of desperation” to an aggressive, successful ecosystem land grab.

At $194 USD, institutions are realized they are buying a business with near-90% gross margins, an essential role in enterprise workflows, and a massive capital return program at a valuation usually reserved for distressed cyclicals.

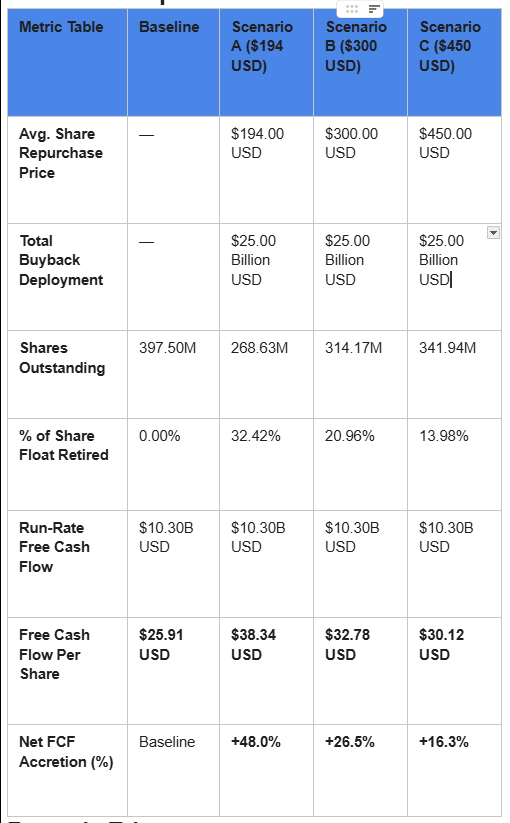

The Three-Scenario Capital Deployment Model

The velocity of Adobe’s financial turnaround is directly tied to the average price at which management executes the $25 billion USD buyback program.

Scenario A: Deep-Value Capitulation (Avg. Execution: $194.00 USD)

In this scenario, negative sentiment persists for an extended period, allowing management to exhaust the full $25 billion USD authorization at or near current multi-year lows.

Shares Repurchased: 128.87 million shares

Remaining Float: 268.63 million shares

Total Share Count Reduction: 32.42%

Post-Buyback FCF per Share: $38.34 USD

Structural FCF Accretion: +48.0%

Scenario B: Mean Reversion / Baseline Recovery (Avg. Execution: $300.00 USD)

In this scenario, a stabilization of leadership and initial clarity around AI freemium conversion triggers a moderate recovery, meaning the buyback is executed evenly as the stock moves up toward its historical baseline.

Shares Repurchased: 83.33 million shares

Remaining Float: 314.17 million shares

Total Share Count Reduction: 20.96%

Post-Buyback FCF per Share: $32.78 USD

Structural FCF Accretion: +26.5%

Scenario C: Rapid Re-rating / Growth Bull Case (Avg. Execution: $450.00 USD)

In this scenario, aggressive operational beats cause the equity price to jump quickly. Management completes the buyback program at a much higher average multiple, reducing the structural efficiency of the deployment.

Shares Repurchased: 55.56 million shares

Remaining Float: 341.94 million shares

Total Share Count Reduction: 13.98%

Post-Buyback FCF per Share: $30.12 USD

Structural FCF Accretion: +16.3%

Forensic Takeaway

The quantitative reality explains why fund managers are building positions. An asset yielding over 13% in free cash flow is a rarity in the large-cap technology space.

If the share price stays depressed near $194.00 USD, Adobe can retire nearly one-third of its entire company using existing capital authorizations. This massive reduction in share count automatically creates a 48% structural lift to FCF per share, providing institutional investors with a robust fundamental floor even if top-line revenue growth temporarily slows down during the leadership transition.

*Disclaimer: The financial analysis, valuations, and metrics presented in this report are for informational, analytical, and educational purposes only. This content does not constitute financial, legal, or investment advice, nor does it represent a formal solicitation to buy or sell securities. Past performance is not indicative of future market results.*